I am tracking this thread… I have desire to use dhan data/option chain and such rendering/data integrity issues especially w.r.t option greeks can lead to chaos.

Hey @displayflex, the difference you see in delta across brokers is mostly because each one uses slightly different models, volatility inputs, or pricing methods, so the values may not always match exactly.

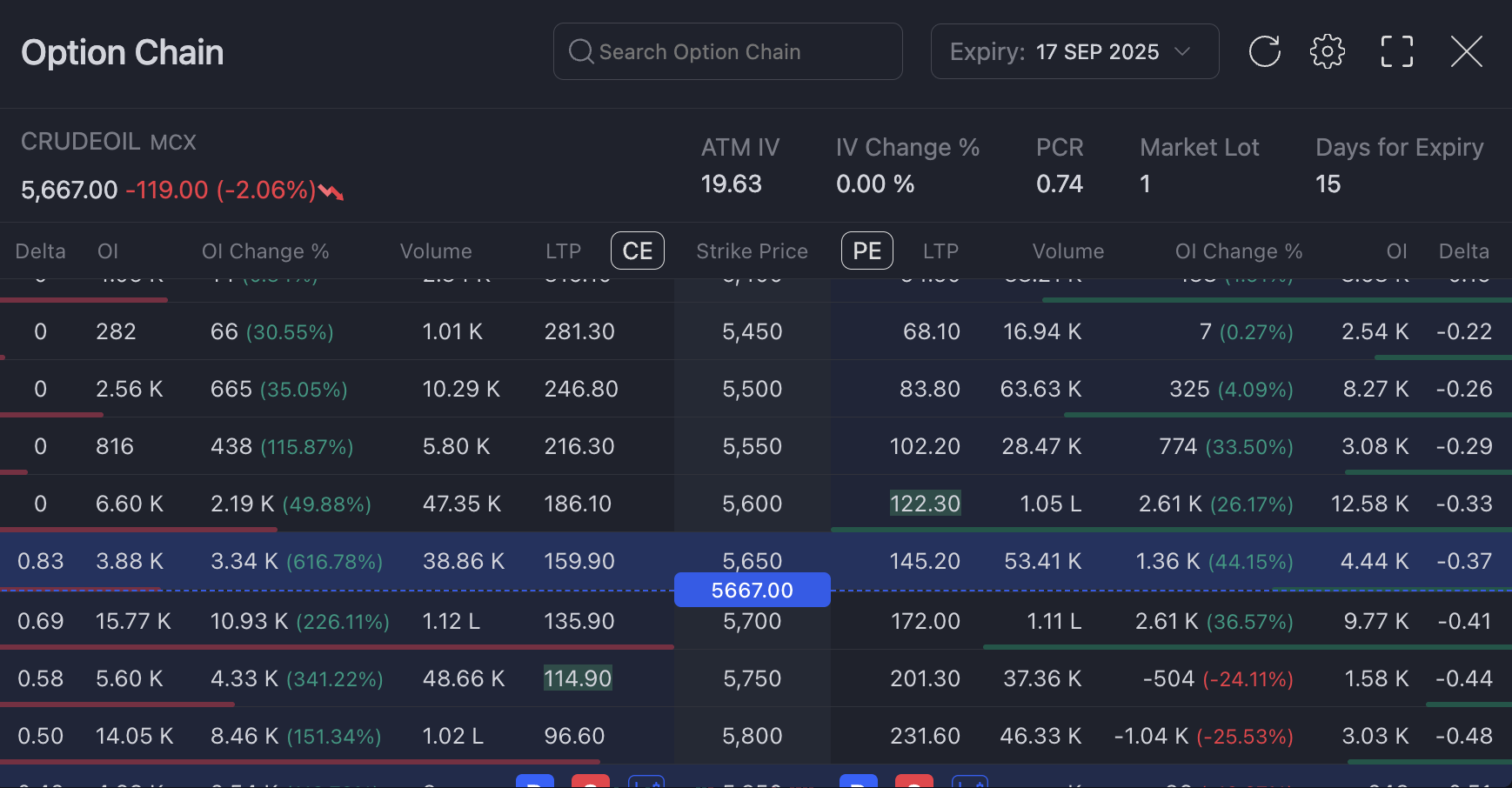

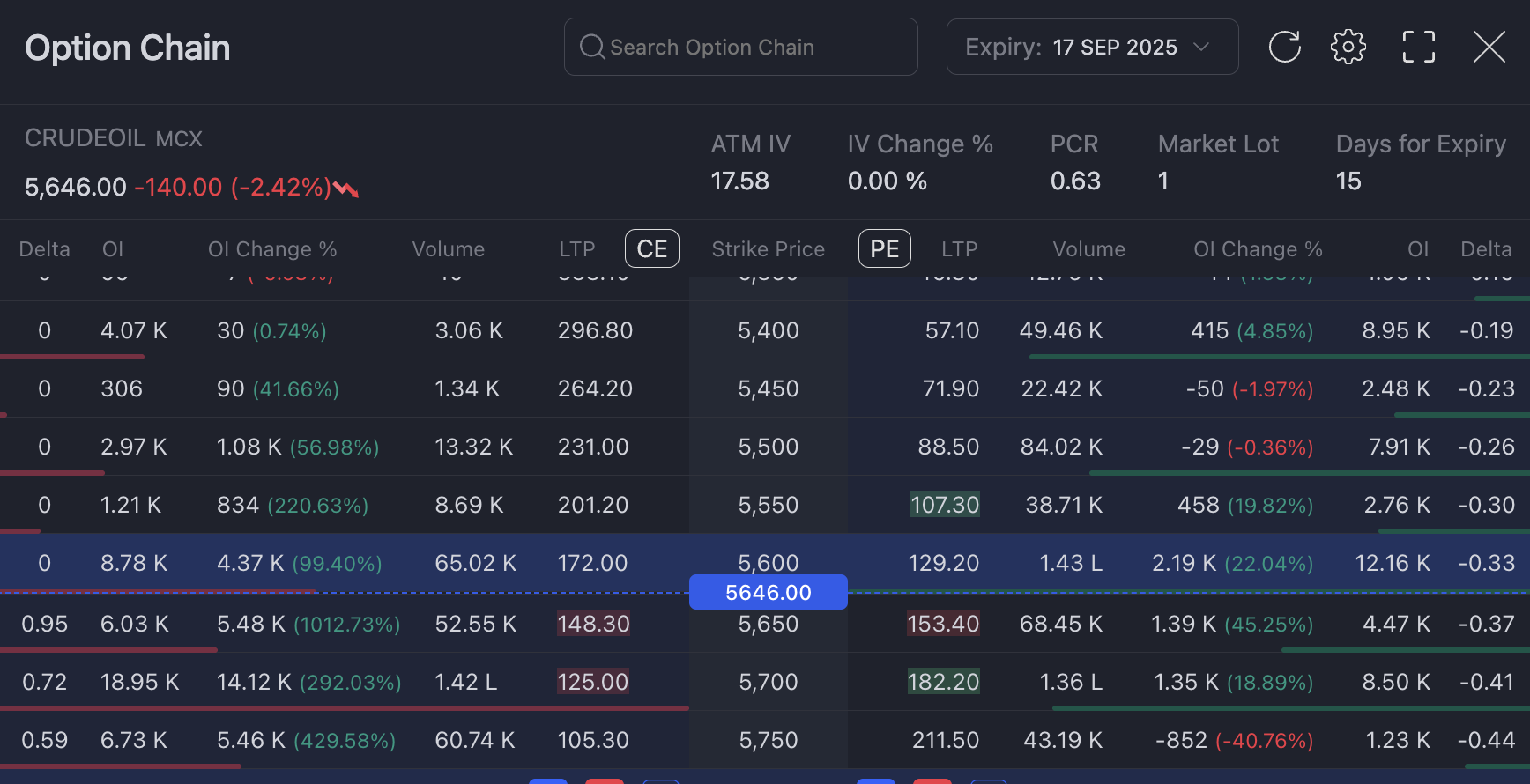

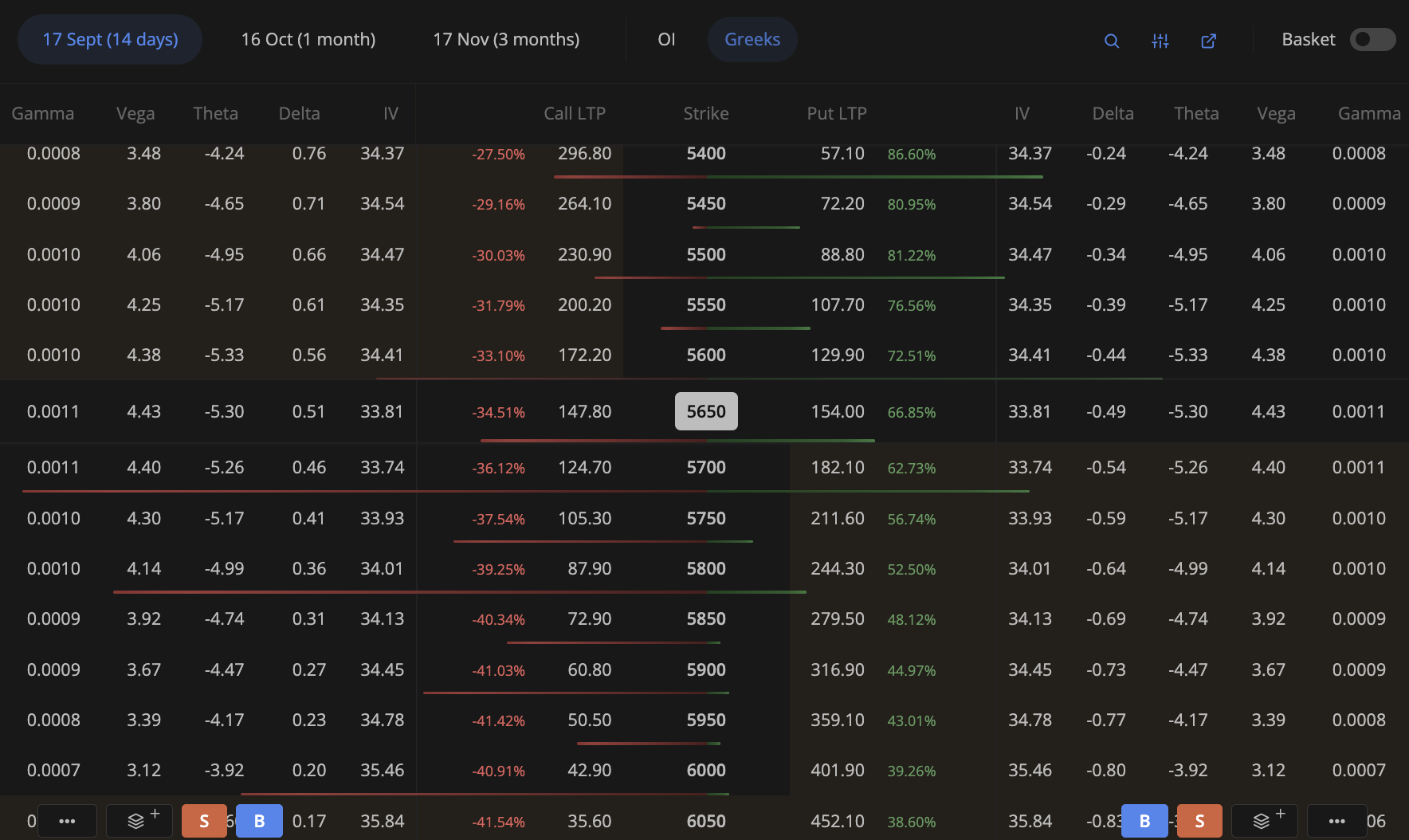

Can the delta of an options instrument at ATM be outside the range of -.5 and +.5 ?

No, the delta of an at-the-money (ATM) options instrument is typically within the range of -0.5 to +0.5, and it should not be outside this range under normal market conditions.

Here’s why:

Call options have positive delta (between 0 and +1).

Put options have negative delta (between -1 and 0).

For ATM options, the underlying price is very close to the strike price, so:

An ATM call option typically has a delta ≈ +0.5

An ATM put option typically has a delta ≈ -0.5

This reflects the fact that there’s about a 50% chance the option will finish in the money.

So, is it possible for ATM delta to be outside of -0.5 to +0.5?

Only in special or non-standard cases, such as:

American options with early exercise potential (e.g., on dividend-paying stocks):

The delta might be slightly higher than 0.5 for calls, or lower than -0.5 for puts, especially near ex-dividend dates.

Deep volatility skew or smile:

Sometimes, implied volatility curves are heavily skewed, which can cause slight shifts in delta. But this typically affects OTM/ITM options more than ATM.

Exotic options:

Certain exotic or path-dependent derivatives (like barrier options) may have unusual delta behavior, but these aren’t plain vanilla options.

Hi @displayflex, we tried reaching you for a call but were unable to connect.

Please note that Delta values are calculated based on the underlying asset’s movement. The differences you see across brokers are usually due to variations in models, volatility inputs, or pricing methods used by each platform, so the values may not always match exactly.

Kindly reach us via support if you need further clarification.