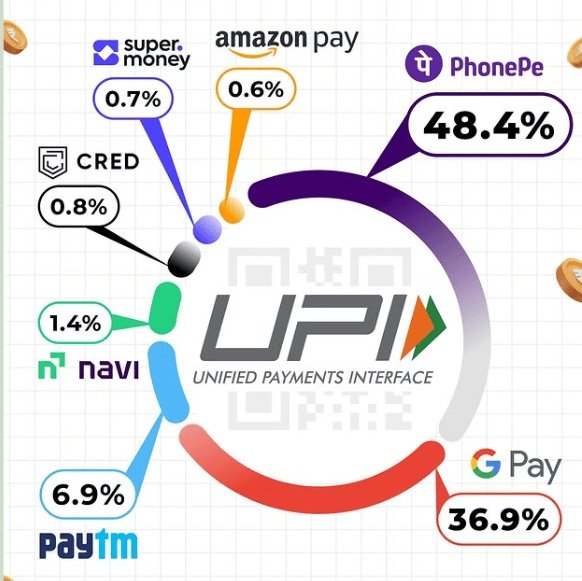

Came across this chart today and it tells a very interesting story about the UPI ecosystem.

Top 2 controls more than 85 percent of the entire UPI market. this is a clear example of a duopoly.

Even though UPI is open and free to use, the market naturally shifted toward a winner-takes-most model. This usually happens because of:

1. Network effects

The more people use a payments app, the more valuable it becomes. When family, friends and shops are all on the same platforms, usage grows even faster.

2. User experience

The dominant apps entered early, offered simple design, fast payments and low failure rates. A smooth experience quickly builds trust.

3. Habit and switching cost

Once users link bank accounts and use an app daily, they rarely switch unless something goes wrong.

This shows how even free and open systems can slowly create monopoly or duopoly structures simply through user behaviour.

I’m currently using SuperMoney in recent months and it has been smooth so far. Curious to know which platform others here prefer for UPI.

Also would like to know if Dhan plans to add UPI on its platform in the future. Interestingly, even Groww doesn’t appear in UPI share despite having a massive user base.